EVALUATE YOUR EXISTING DISABILITY COVERAGE in only 5 minutes

EVALUATE YOUR EXISTING DISABILITY COVERAGE in only 5 minutes*ICBC is a Crown Corporation but is still included in the below chart to simplify the comparison.

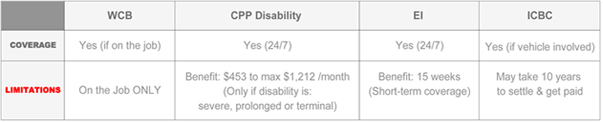

GOVERNMENT INCOME REPLACEMENT PROGRAMS

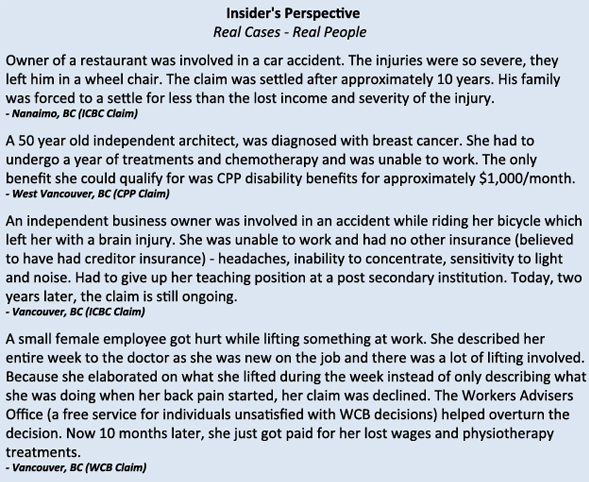

ICBC The Insurance Corporation of BC could make you wait 10 years before they offer a reasonable settlement. For many claimants, a reasonable settlement may never come and in the absence of other insurance, they are often forced to settle for less than they deserve. Technically speaking, a claim through ICBC does not pay out income replacement but is usually a lump sum benefit which accounts for actual lost income to date in addition to estimated future income loss (settlements also include coverage for medical bills, etc.,). If your injury is minimal, the claim maybe settled within 6 months. If your injury is more serious, most lawyers recommend not to settle until you have recovered from the condition entirely.

WCB The Workers Compensation Board will re-evaluate your wage loss benefit as soon as your condition is stable, whether or not you can return to work. After the review, your benefit will be reduced by what “they believe” you can earn in any other occupation, whether or not such a job is available for you. Let’s not forget that you will have to prove that the injury was sustained at work. All in all, WCB wording is such that it provides for good, comprehensive short-term benefit while in recovery from a workplace injury.

EI Employment Insurance provides for a 15 week benefit. As a contractor, you have the option to opt into the plan and make a commitment to participate for as long as your are self-employed. There is also a minimum contribution before you would be eligible to claim this 15 week sickness/injury benefit. The payout for eligible contractors is 55% of insurable earnings up to a maximum of $524/week. For more information, refer to Employment Insurance for Self-Employed People.

CPP Disability The Canadian Pension Plan Disability coverage is paid out in the event of prolonged, severe and/or terminal disability. Eligibility and benefits are based on the number of years you contributed to CPP. You would be eligible at least for some benefits, if you contributed for 4 out of the last 6 years or alternatively 3 out of 6 for those who have made contributions for a minimum of 25 years. The maximum benefit payable to anyone is approxiamtely $1,212 per month (May, 2015).

For most of these claims, unless you have a private disability policy in place, you will receive Employment Insurance (if you are eligible) for 15 weeks and then transition to CPP disability benefits for about $1,000/month only if your disability is severe, prolonged or terminal.

WHAT IS YOUR RISK EXPOSURE?

The most common disability claims inadequately covered by any government programs exposing contractors to great financial risks include:

- Musculoskeletal/connective tissue disorders account for 30% of disability claims

- Disorders of the nervous system and sense organs account for 14% of disability claims

- Cardiovascular/circulatory disorders account for 12% of disability claims

- Cancer accounts for 9% of disability claims

- Mental disorders account for 7% of disability claims

PRIVATE DISABILITY INSURANCE PROGRAMS (Optional)

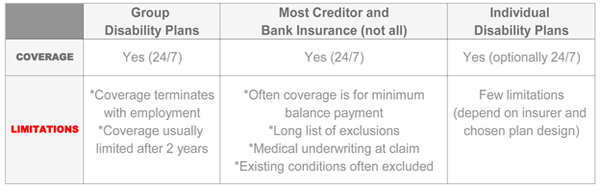

Group Disability Plans are not usually available to contractors. On occasion, contractors maybe given the option to join a group plan for all benefits and pay 100% of their own premium. It is recommended to consult with a tax lawyer prior to proceeding to enroll in a group plan as a contractor to ensure your contractor status is not impacted. If covered under a group plan, the most common plan design will provide coverage for an individual who is unable to do their regular occupation for 2 years. Thereafter, the definition changes to ”any occupation”. This means that benefits will cease should that individual be able to do any other occupation in which they can earn 50% of their pre-disability earnings.

Creditor and Bank Disability Insurance is usually very limited in coverage. It is especially important that you request a copy of your policy and see what is actually covered. Many such policies will only cover the required minimum payment. Others might require your medical file and deny your claim if the disability is a result from a pre-existing medical condition.

Individual Disability Plans are your only alternative if you want to have control over your coverage and financial security. They are customizable with sometimes up to 30 optional upgrades for more comprehensive coverage. So even though individual insurance maybe the best alternative, not all individual policies are created equal. Some policies are very comprehensive without many upgrades. Others, start out with the very basic coverage and have a long list of limitations and exclusions. Common exclusions include: Soft tissue injuries, Mental illnesses, High risk activities, and Chronic pain syndrome which account for close to 50% of disability claims. It is always recommended to read and understand the definitions, exclusions and limitations of your policy.

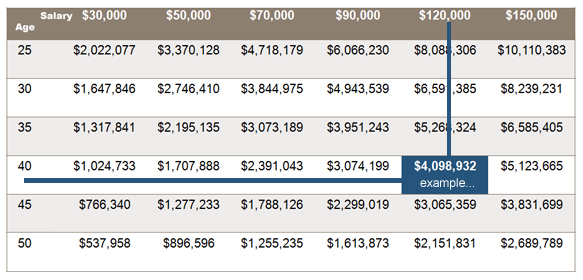

HOW MUCH INCOME ARE YOU GOING TO EARN BY AGE 65? (inflation factor included)

How much is 4,000,000 of earnings over a life time worth? $50/month? $100/month? Accident onlydisability insurance cost starts at as little as about $30/month for a $2,000/month benefit. Financials are not required at sign-up but are often required at claim. This rate varies slightly with occupation but not with age since it is for accidents alone. Other, more flexible options including illness insurance and higher coverage amounts are also available through various providers. At Brightin-Insider, we are independent and work with all insurance carriers. As such, we survey the market to find the best solutions able to meet each of our clients’ needs.

CUSTOMIZED INSURANCE AND WEALTH GENERATION PLANNING

With our customizable individual and corporate insurance packages, we provide our clients with personalized and yet unbiased insurance advice and solutions. Our services enable contractors to achieve their individual goals, ensure their financial independence and retirement security. We are independent of any one insurance company and have access to the entire market place. And as aforementioned, we survey the market to find the best solutions able to meet each of our client’s needs.

With our customizable individual and corporate insurance packages, we provide our clients with personalized and yet unbiased insurance advice and solutions. Our services enable contractors to achieve their individual goals, ensure their financial independence and retirement security. We are independent of any one insurance company and have access to the entire market place. And as aforementioned, we survey the market to find the best solutions able to meet each of our client’s needs.

Free Planning Sessions & Seminars:

- RRSP regular contribution strategies

- Creditor protected wealth and legacy building strategies.

Book a free 30 minute consultation or attend one of our free seminars to find out more.